The Trillion-Dollar Question

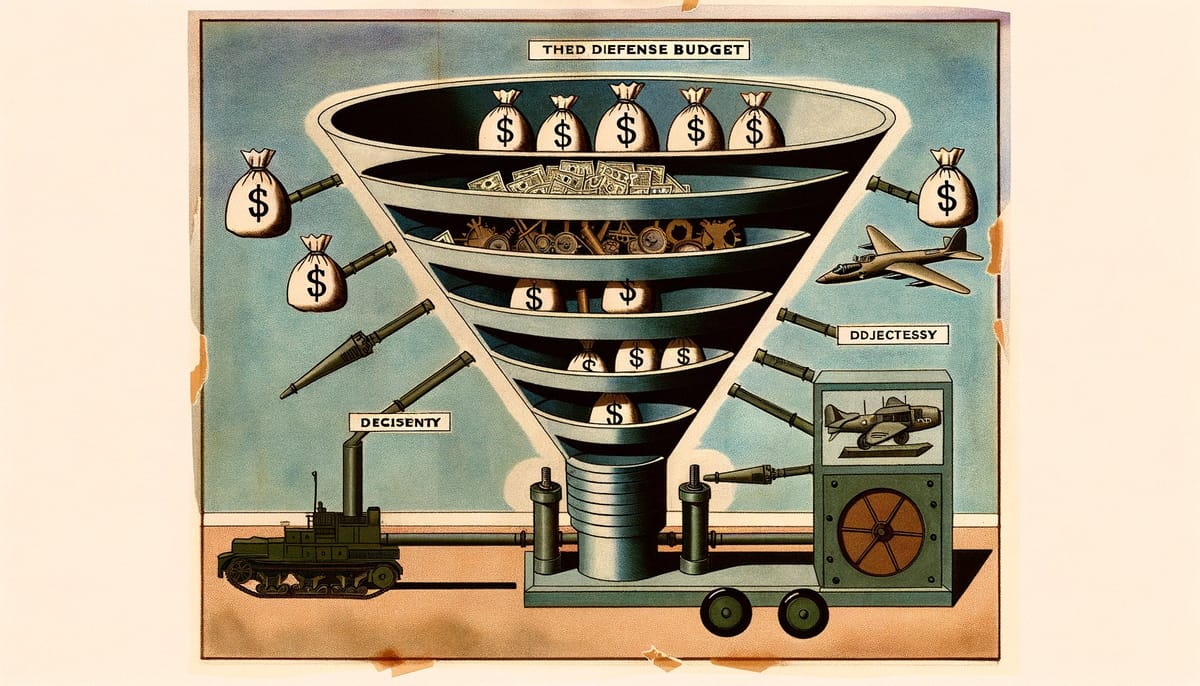

President Trump's call for a 50% defense budget increase promises to fix America's military readiness crisis. But the system that converts dollars into capability is broken. More money through broken channels produces contractor profits, not combat power.

The Trillion-Dollar Question

In January 2026, President Trump called for a $1.5 trillion defense budget—a 50% increase over current levels. The proposal landed with the subtlety of a cruise missile. Pentagon officials praised it as “historic.” Defense contractors’ stock prices jumped. And somewhere in a congressional hearing room, the same debate that has played out for six decades began again: would the money actually make America safer, or would it simply flow to Lockheed Martin’s shareholders?

The question is not rhetorical. The Government Accountability Office reports that U.S. military readiness “has been degraded over the last two decades.” The Heritage Foundation rates American military posture as “weak” for the second consecutive year, warning of “significant risk” in a major conflict. Ships sit in maintenance backlogs. Aircraft miss flight hours. Ammunition stockpiles look thin after Ukraine consumed years of production in months.

Yet from 2020 to 2024, the top five defense contractors received $771 billion in Pentagon contracts—one-third of all defense spending—while converting improved profit margins into 73% higher shareholder payments rather than expanded production capacity. The money flowed. The readiness didn’t follow.

What Readiness Actually Means

Begin with definitions. “Readiness” in Pentagon doctrine means the ability of military forces to fight and meet assigned missions. It encompasses personnel, equipment, training, and logistics. A ready force can deploy on short notice and sustain operations. An unready one cannot.

The current crisis is real, not manufactured. The GAO documents persistent aircraft maintenance backlogs, personnel shortages, and aging equipment across services. The Navy’s fleet readiness hovers around 68%. The Army’s depot maintenance backlog stretches into years. When Ukraine began firing 6,000 artillery shells daily against Russia’s 20,000, it exposed a production base that had been optimized for peacetime efficiency rather than wartime surge.

But readiness problems have specific causes. High operational tempo since 2001 wore down equipment faster than it could be replaced. Deferred maintenance accumulated like compound interest—each year’s shortfall making the next year’s problem worse. Training pipelines couldn’t keep pace with attrition. And the industrial base consolidated from 51 aerospace and defense prime contractors in the 1990s to just five today, reducing the competition that traditionally spurred innovation and lowered costs.

A budget increase addresses none of these structural problems directly. More money flowing through the same channels will encounter the same bottlenecks. The question is not whether America spends enough on defense. It is whether the spending system can convert dollars into capability.

The Consolidation Trap

Consider the defense industrial base. The Pentagon’s own assessment concluded that consolidation has “reduced competition” with fewer bidders per program and more sole-source contracts. This matters because monopoly and oligopoly suppliers face different incentives than competitive ones. They can charge higher prices. They can underinvest in capacity. They can prioritize shareholder returns over production expansion.

The evidence suggests they do exactly that. Defense contractor capital expenditure and R&D investment declined even as profits rose between 2000 and 2019. The money that might have built new factories or developed new manufacturing processes instead funded dividends and stock buybacks. When demand surged after Ukraine, the industrial base lacked the capacity to respond. Artillery shell production couldn’t scale. Missile inventories couldn’t replenish.

A 50% budget increase would pour more money into this same concentrated structure. The five major primes—Lockheed Martin, RTX, Boeing, General Dynamics, and Northrop Grumman—would absorb the bulk of new contracts. Their shareholders would benefit. Their production lines might expand marginally. But the fundamental dynamic of monopoly pricing and underinvestment would persist.

The medieval guild system offers an unexpected parallel. Guilds maintained monopolies by legally prohibiting non-members from practicing trades within city boundaries. Defense primes maintain monopolies through a different mechanism: proprietary technical data, security clearances, and the sheer complexity of regulatory compliance that only large firms can navigate. The 30-plus layers of management paperwork documented in acquisition reform studies function as a barrier to entry, not quality control.

Small contractors who once provided “most affordable and highest quality” work increasingly refuse to bid. The compliance burden exceeds their capacity. The system selects for size over efficiency.

The Acquisition Labyrinth

Money enters the Pentagon through one of five appropriation categories: personnel, operations and maintenance, procurement, research and development, and military construction. Each follows different rules. Each creates different incentives.

The “full funding policy” for procurement requires entire acquisition costs to be budgeted upfront in the year of purchase. This creates a structural bias toward visible, discrete platform purchases—new aircraft, new ships, new vehicles—that can be ribbon-cut and photographed. Meanwhile, operations and maintenance funding, which sustains existing equipment, competes for whatever remains. The result: America buys new platforms it cannot afford to maintain.

The F-35 program exemplifies the pattern. The GAO’s September 2025 assessment found costs “over $6 billion more and completion at least five years later than original estimates.” All 110 aircraft delivered in 2024 arrived late by an average of 238 days. The program absorbs vast sums while readiness metrics for existing aircraft decline.

This is not corruption in the conventional sense. No one is stealing money. The system works exactly as designed—it just wasn’t designed to maximize readiness. It was designed to spread contracts across congressional districts, to provide stable employment in defense communities, to give contractors predictable revenue streams, and to give politicians ribbon-cutting opportunities. Readiness is a byproduct, not the objective.

A 50% budget increase would flow through this same acquisition system. The two-year appropriation window for research and development creates incentives to fund contractor-led prototypes rather than slow-maturing organic capabilities. The preference for new procurement over maintenance would persist. The bias toward large platforms over ammunition and spare parts would continue.

The Temporal Mismatch

Military readiness operates on multiple timescales that budget cycles cannot accommodate. Training a cyber operator takes 50 weeks. Building a new shipyard takes a decade. Developing institutional knowledge in a depot workforce takes a generation. Annual appropriations cannot address problems that unfold across years.

The research reveals a striking pattern: Presidential Drawdown Authority operates at crisis tempo—hours to days—while industrial base replenishment operates at geological tempo—years to decades. When the administration rapidly transfers weapons to Ukraine, it creates obligations that the industrial system must labor under for years. The faster we can legally commit stockpiles, the longer the production system struggles to catch up.

Steel corrosion follows exponential acceleration: once protective layers breach, pitting depth increases non-linearly. Ships and aircraft degrade the same way. Deferred maintenance doesn’t accumulate linearly—it compounds. The $50-80 billion maintenance backlog understates the true cost because each year of deferral accelerates future degradation.

Budget systems model maintenance as discrete repair events. Thermodynamic reality operates continuously. This mismatch cannot be solved by adding money. It requires restructuring how money flows through time.

The Contractor Dependency Spiral

The transition from organic military maintenance to contractor depot maintenance optimized for peacetime efficiency but eliminated surge capacity. Contractors price specific repair tasks rather than maintaining latent capability across multiple platforms. When demand spikes, no slack exists in the system.

This creates what biologists call “phase-locked” dynamics. As the Department of Defense reduces organic maintenance capacity, contractor dependency increases. As contractor dependency increases, the knowledge required to perform maintenance in-house erodes. As institutional knowledge erodes, returning to organic maintenance becomes progressively more difficult. The system locks into a stable but suboptimal equilibrium.

Experienced welders who join the military express regret. Their craft knowledge flows back to civilian welder networks as negative signals about military work conditions. This creates a transmission mechanism that degrades the talent pipeline. The 50-week cyber training pipeline cannot compete with private sector salaries. The depot workforce ages without replacement.

A budget increase could theoretically address these problems—higher military pay, better facilities, more training slots. But the acquisition system’s preferences would redirect funds toward procurement rather than personnel and training. The same structural biases that created the readiness crisis would shape how new money gets spent.

What Would Actually Work

Three intervention points offer genuine leverage. Each requires sacrifice.

First, break the prime contractor oligopoly. The Pentagon could mandate competition by splitting large programs into smaller contracts that mid-tier firms can bid on. This would sacrifice economies of scale and the convenience of single-throat-to-choke accountability. Program management would become more complex. But it would restore the competitive dynamics that once drove innovation and controlled costs.

Second, restructure appropriations to favor sustainment over acquisition. Congress could mandate that a fixed percentage of defense spending flow to operations, maintenance, and ammunition before new platforms. This would sacrifice the ribbon-cutting opportunities that politicians crave. Fewer new aircraft would mean fewer factory jobs in key districts. But it would address the actual readiness crisis rather than the symbolic one.

Third, rebuild organic maintenance capacity. The military could reclaim depot work from contractors, accepting higher peacetime costs in exchange for surge capability. This would sacrifice short-term efficiency for long-term resilience. Contractors would fight it. Congressional delegations with contractor facilities would resist. But it would break the phase-locked dependency spiral.

None of these interventions requires a 50% budget increase. All of them require political will that has been absent for decades.

The Most Likely Outcome

A 50% budget increase will not happen as proposed. Even Trump’s own party balked at the fiscal implications. The actual FY2027 budget will likely land somewhere between current levels and the aspirational target—perhaps a 10-15% real increase.

This money will flow through existing channels. Procurement will absorb the largest share. The prime contractors will book higher revenues. Shareholder payments will increase. Some marginal expansion of production capacity may occur, particularly for ammunition that Ukraine’s consumption highlighted as critically short.

Readiness metrics may improve slightly. More flying hours. Faster ship repairs. Fuller ammunition bunkers. But the structural problems—consolidation, acquisition dysfunction, temporal mismatch, contractor dependency—will persist.

The readiness crisis is real. The proposed solution is not a solution. It is a ritual—the same ritual that has been performed every time readiness concerns surface, producing the same results. Money flows. Contractors profit. Readiness remains “weak.”

The question is not whether to spend more on defense. It is whether America can reform the institutions that convert spending into capability. Until that question receives a serious answer, additional billions will produce additional contractor profits without producing additional security.

FAQ: Key Questions Answered

Q: How much does the U.S. currently spend on defense? A: The current defense budget sits around $850-890 billion annually. Trump’s January 2026 proposal for $1.5 trillion would represent approximately a 50% increase from this baseline.

Q: What is the defense industrial base, and why does consolidation matter? A: The defense industrial base comprises the companies that manufacture weapons, equipment, and supplies for the military. Consolidation from 51 prime contractors to 5 since the 1990s has reduced competition, leading to higher prices, less innovation, and underinvestment in production capacity.

Q: Why can’t the military just produce more ammunition quickly? A: Production capacity was optimized for peacetime efficiency, not wartime surge. The U.S. produced 240,000 artillery shells annually before Ukraine—barely 40 days of Ukrainian consumption. Expanding capacity requires new factories, trained workers, and supply chains that take years to build.

Q: Do defense contractors actually make excessive profits? A: Between 2020 and 2024, the top five contractors received $771 billion in contracts while increasing shareholder payments by 73% and reducing capital investment. Whether this constitutes “excessive” profit depends on one’s perspective, but it clearly prioritized returns over capacity expansion.

The Ledger That Matters

The debate will continue in familiar terms. Hawks will cite threat assessments and demand more spending. Doves will cite contractor profits and demand reform. Both will be right about the facts and wrong about the conclusion.

The readiness crisis exists because the system that converts money into military capability is broken. More money through a broken system produces more of what the system already produces: contractor profits, program delays, maintenance backlogs, and PowerPoint briefings about transformation that never arrives.

Somewhere in a depot in Oklahoma, a skilled technician is retiring without a replacement. Somewhere in a shipyard in Virginia, a vessel waits for parts that won’t arrive for months. Somewhere in a congressional hearing room, a general is requesting more funding for a program that will deliver late and over budget.

The trillion-dollar question has a trillion-dollar answer: it depends on what you’re buying. America is buying the same defense system it has always bought. The results will be the same results it has always gotten.

Sources & Further Reading

The analysis in this article draws on research and reporting from:

- GAO Military Readiness Assessment (GAO-24-107463) - comprehensive review of degraded readiness across services

- Pentagon State of Competition Report - official assessment of industrial base consolidation

- Quincy Institute “Profits of War” Report - analysis of contractor revenues and shareholder returns

- GAO F-35 Assessment (GAO-25-107632) - documentation of program delays and cost overruns

- War on the Rocks: Rethinking Defense Acquisition - analysis of regulatory burden in procurement

- DAU Acquisition Life Cycle Wall Chart - official reference for appropriation and acquisition timelines

- MERIP: Defense Industry’s Role in Militarizing Foreign Policy - examination of contractor influence on policy