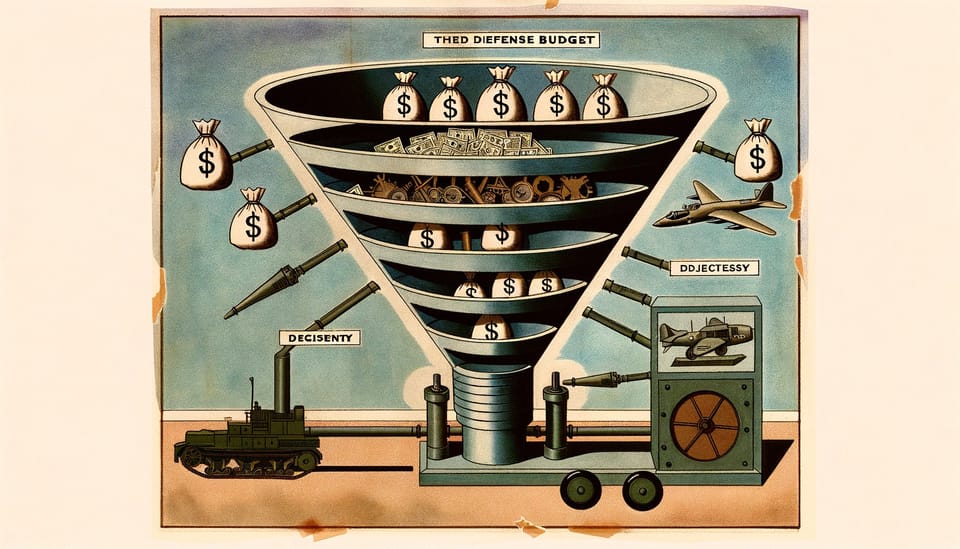

The Trillion-Dollar Bottleneck

Trump's proposed 50% defence spending surge promises a 'Dream Military' by 2027. But with the industrial base running at 41% capacity and 700,000 security clearances backlogged, the money cannot buy what the factories cannot build. The bottleneck is physical, not fiscal.

The Trillion-Dollar Bottleneck

America’s defence industrial base operates at 41% capacity utilization—the lowest of any major manufacturing sector. This is not a funding problem. It is a physics problem.

President Trump’s call for $1.5 trillion in defence spending by 2027 represents the largest proposed military budget surge since the Reagan buildup. The headline figure—a 50% increase from the $901 billion Congress approved for 2026—has triggered predictable responses: hawks celebrate, doves despair, and defence contractors quietly update their investor presentations. Yet the central question remains unasked in Washington’s spending debates: can the industrial base actually absorb this money?

The answer, based on the structural dynamics of American defence production, is troubling. More dollars chasing constrained capacity does not accelerate delivery. It inflates costs. The bottleneck is not in appropriations committees but in welding bays, machine shops, and the minds of workers who no longer exist in sufficient numbers. Trump’s surge risks becoming the most expensive demonstration in history that money cannot buy what the industrial base cannot build.

The Capacity That Isn’t There

The conventional narrative treats defence production as a dial that spending can turn. Appropriate more, produce more. This mental model made sense in 1942, when America possessed vast industrial slack and a workforce eager for manufacturing jobs. It makes no sense in 2026.

Consider the submarine industrial base. The United States operates precisely two shipyards capable of building nuclear submarines: General Dynamics Electric Boat in Connecticut and Huntington Ingalls Newport News in Virginia. Both are running at maximum capacity. The Navy’s own assessments acknowledge that even maintaining current production rates—let alone accelerating them—requires workforce expansions that cannot materialize for years. You cannot train a nuclear-qualified welder in a budget cycle.

The problem compounds upstream. A GAO assessment of major defence acquisition programs found that 30 programs experienced combined cost growth of $49.3 billion, driven by development delays and inflation. The report’s clinical language obscures a damning reality: the Pentagon continues to struggle with delivering innovative technologies quickly and within budget. This is not new. It is structural.

Munitions production illustrates the constraint with brutal clarity. When Russia invaded Ukraine, America’s annual artillery shell production stood at 240,000 rounds—barely 40 days of Ukrainian consumption at wartime rates. The surge to 100,000 rounds monthly by 2025 required years of investment, new production lines, and workforce recruitment. Even this expanded capacity remains inadequate for a major peer conflict. The 155mm shell surge succeeded because the technology is mature and the production process well-understood. Hypersonic weapons tell a different story: three successive Air-launched Rapid Response Weapon failures between 2019 and 2022 demonstrated that throwing money at immature technologies accelerates nothing except embarrassment.

The workforce crisis runs deeper than headlines suggest. Aerospace and defence turnover now matches Silicon Valley’s 13.2% annual churn—but submarines take a decade to build, not a sprint cycle. Welders and machinists with security clearances cannot be conjured from coding bootcamps. The clearance backlog alone exceeds 700,000 cases, with top-secret processing now taking 70 days longer than historical norms. Workers awaiting clearance draw salaries but produce nothing. This creates a perverse premium: already-cleared workers command 5-15% higher wages, bidding up costs without expanding output.

Regional labour immobility compounds the shortage. American workers no longer move for jobs the way they once did. Home attachment, dual-income households, and housing cost differentials trap skilled workers in regions distant from defence production centres. The shipyard cities and arsenal towns that once attracted mobile labour now compete for a shrinking pool of workers who refuse to relocate. Defence surge spending concentrates in specific locations, but the workers do not follow the money.

The Acquisition Labyrinth

If workforce constraints form one wall of the bottleneck, acquisition regulations form the other. The Pentagon’s procurement system was designed for a different era—one where time mattered less than avoiding scandal, where process legitimacy trumped delivery speed.

The Weighted Guidelines Method, established in 1964, determines contractor profit rates through a formula that mimics rational calculation without connecting to actual value delivery. Like cargo cult rituals that replicate the form of aircraft to summon cargo, the method produces numbers that satisfy bureaucratic requirements while bearing no relationship to production efficiency. Contractors optimize for compliance, not capability.

Multi-year procurement contracts were explicitly designed in 1981 as a solution to defence industrial base erosion. Four decades later, the National Defense Industrial Association reports that these same policies led to boom-bust cycles and drastic consolidation. The solution became the problem. Contractors learned to extract maximum profit during boom phases while shedding capacity during busts, knowing that desperate future surges would reward survivors with monopoly pricing power.

The compliance barrier has become a geographic sorting mechanism. CMMC 2.0 cybersecurity requirements, cost accounting systems, and domestic content rules demand pre-investment in compliance infrastructure before companies can even bid on contracts. Small manufacturers in regions distant from defence hubs cannot afford this entry cost. The result: production concentrates among fewer firms in fewer locations, reducing the very surge capacity that wartime would require.

Acquisition reform efforts have produced impressive acronyms and minimal results. The Adaptive Acquisition Framework promised flexibility. Middle-Tier Acquisition authorities promised speed. Software acquisition pathways promised relevance. Yet GAO’s persistent findings document the same patterns: cost growth, schedule delays, performance shortfalls. The system resists reform because the incentives that created it remain unchanged. No programme manager was ever fired for following process. Many have been fired for taking risks that failed.

The Consolidation Trap

America’s defence industrial base has consolidated into a structure that maximizes peacetime efficiency and minimizes wartime adaptability. Five prime contractors dominate major systems. Below them, a fragile lattice of subcontractors and specialty suppliers operates on margins too thin to maintain excess capacity.

This consolidation was deliberate policy. Post-Cold War drawdowns encouraged mergers to reduce overhead. The “Last Supper” of 1993, when Deputy Secretary of Defence William Perry told industry executives to consolidate or die, produced exactly the oligopoly that now constrains production. The primes that survived—Lockheed Martin, Raytheon, Northrop Grumman, Boeing, General Dynamics—learned that market power matters more than manufacturing prowess.

Between 2017 and 2020, defence contractors spent 76% of free cash flow on stock buybacks and dividends rather than capacity expansion. This was rational behaviour under existing incentives. Treating a surge as permanent would create fixed costs that become politically impossible to shed when the surge ends. Better to extract cash, reward shareholders, and wait for the next crisis to justify premium pricing.

Trump’s executive order demanding that contractors end buybacks and cap executive pay until they invest in manufacturing capacity addresses symptoms, not causes. The underlying dynamic—a monopsony buyer facing an oligopoly of suppliers—creates structural incentives for extraction over investment. Contractors know that the government cannot credibly threaten to take production elsewhere. There is no elsewhere.

The subcontractor lattice exhibits a particularly dangerous vulnerability. The most connected nodes—experienced machinists, specialty shops with rare capabilities—are simultaneously the oldest and least replaceable. When a 62-year-old toolmaker retires, the knowledge encoded in his hands retires with him. No amount of appropriated dollars can purchase what no longer exists.

The Thermodynamics of Defence Spending

Defence spending operates under constraints that resemble thermodynamic laws more than economic ones. Energy cannot be created or destroyed, only transformed. Similarly, money appropriated for defence cannot create capacity that does not exist—it can only bid up prices for capacity that does.

When demand exceeds supply in a constrained market, prices rise. This is not waste or fraud. It is physics. A 50% spending increase chasing 41% capacity utilization does not produce 50% more weapons. It produces the same weapons at higher prices, with contractors capturing the difference as profit.

The historical parallel is instructive. Reagan’s defence buildup succeeded partly because it inherited industrial slack from the 1970s recession and a workforce still oriented toward manufacturing careers. The current surge inherits neither. Manufacturing employment has declined for decades. Young workers pursue coding bootcamps, not welding certifications. The cultural infrastructure that once channelled talent toward production has atrophied.

Some spending can expand capacity over time. New production lines, workforce training programmes, and supplier development initiatives eventually increase output. But the lag between appropriation and production stretches across years, not budget cycles. A dollar appropriated in 2027 might produce a weapon in 2032. For threats that materialize before then, the spending arrives too late to matter.

The Pentagon’s own National Defense Industrial Strategy acknowledges this temporal mismatch. It calls for incentives to maintain spare production capacity during peacetime—but admits that neither the federal government nor investors currently have strong incentives to maintain such capacity. The strategy identifies the problem without solving it.

What Actually Accelerates Delivery

If raw spending cannot solve production bottlenecks, what can? The answer lies in structural interventions that expand capacity rather than merely funding it.

First, workforce development requires investment measured in decades, not appropriations cycles. The nuclear submarine programme’s success rests on a workforce culture that takes years to build—what researchers studying high-reliability organisations call the intersection of several different cultures where formality and informal knowledge coexist and mutually reinforce each other. This cannot be purchased. It must be grown.

Second, acquisition reform must change incentives, not just processes. Contractors respond to profit signals. If the government wants capacity investment, it must make capacity investment profitable. This means multi-year contracts with genuine commitment, not the year-to-year uncertainty that currently discourages capital expenditure. It means accepting that surge capacity costs money to maintain even when unused.

Third, supply chain resilience requires mapping and investment in the subcontractor lattice before crisis reveals its fragility. The ghost network of specialty suppliers operates invisibly until a critical node fails. By then, the knowledge has retired or died. Proactive investment in supplier development and knowledge transfer could preserve capabilities that no amount of crisis spending can recreate.

Fourth, allied production capacity offers the only realistic path to rapid surge. AUKUS submarine cooperation, NATO munitions initiatives, and bilateral production agreements with Japan and South Korea can access capacity that domestic bottlenecks constrain. But this requires accepting that some production will occur outside American borders—a political concession that conflicts with reshoring rhetoric.

Each intervention carries trade-offs. Workforce investment takes years to yield results. Acquisition reform threatens entrenched interests. Supply chain mapping reveals uncomfortable dependencies. Allied production dilutes domestic employment benefits. There are no costless solutions.

The Likely Trajectory

What will actually happen? History suggests a predictable pattern. Congress will appropriate something less than $1.5 trillion but more than current levels. Defence contractors will report record revenues. Delivery timelines will slip. Costs will grow. GAO will document the failures. The cycle will repeat.

The structural constraints that limit production will remain unaddressed because addressing them requires sustained investment across administrations, bipartisan commitment to unpopular trade-offs, and acceptance that some problems cannot be solved by spending alone. None of these conditions currently obtain.

The surge will produce some additional capability. Munitions stockpiles will grow, though not as fast as appropriations suggest. Some shipyard capacity will expand, though submarines will still take a decade to build. Some workforce training will occur, though not at the scale required.

What the surge will not produce is the “Dream Military” that the rhetoric promises. Dreams do not survive contact with physics. The defence industrial base will absorb the money it can absorb and return the rest as profit to shareholders. This is not corruption. It is the predictable behaviour of a system optimised for extraction rather than production.

The deeper question—whether America can rebuild the industrial capacity it deliberately dismantled over three decades—remains unanswered. The answer requires more than appropriations. It requires a theory of industrial policy that neither party currently possesses, workforce investments that span generations, and acceptance that some capabilities, once lost, cannot be recovered at any price.

Trump’s $1.5 trillion proposal is not a strategy. It is a number. The difference matters.

Frequently Asked Questions

Q: How much would Trump’s defence spending proposal actually cost over time? A: The Committee for a Responsible Federal Budget estimates $5 trillion from 2027-2035, or $5.7 trillion including interest costs. This assumes the elevated spending level becomes the new baseline rather than a one-time surge.

Q: Why can’t defence contractors simply hire more workers to increase production? A: Defence manufacturing requires security clearances (700,000+ backlog), specialised skills that take years to develop, and workers willing to relocate to production centres. The clearance process alone adds months before new hires can contribute, and many skilled trades have lost their training pipelines entirely.

Q: What is defence industrial base capacity utilisation and why does it matter? A: Capacity utilisation measures how much of existing production infrastructure is actively being used. At 41%—the lowest of any major sector—defence manufacturing appears to have slack. But this figure masks the reality that specific bottlenecks (skilled labour, specialised facilities, supplier constraints) prevent the unused capacity from being activated regardless of funding levels.

Q: Could allied countries help solve American production bottlenecks? A: Yes, but with significant constraints. AUKUS, NATO initiatives, and bilateral agreements with Japan and South Korea can access production capacity unavailable domestically. However, technology transfer restrictions, domestic content requirements, and political resistance to offshore production limit how much allied capacity can substitute for American shortfalls.

Sources & Further Reading

The analysis in this article draws on research and reporting from:

- GAO Weapon Systems Annual Assessment 2025 - Primary source for cost growth data and programme performance findings

- GAO Defense Acquisition Reform Report - Analysis of persistent acquisition challenges and reform efforts

- Congressional Research Service: Defense Industrial Base - Overview of DIB structure and recent legislative changes

- High Reliability Organizations research - Framework for understanding workforce culture constraints

- Brookings Institution: Economic Impact of the Opioid Epidemic - Labour market constraints affecting manufacturing workforce

- World Economic Forum: US Labour Mobility - Analysis of geographic immobility affecting workforce availability